Key Takeaways for Employers: The ARPA’s Expanded Sick/Family Medical Leave and COBRA Benefits

April 12, 2021

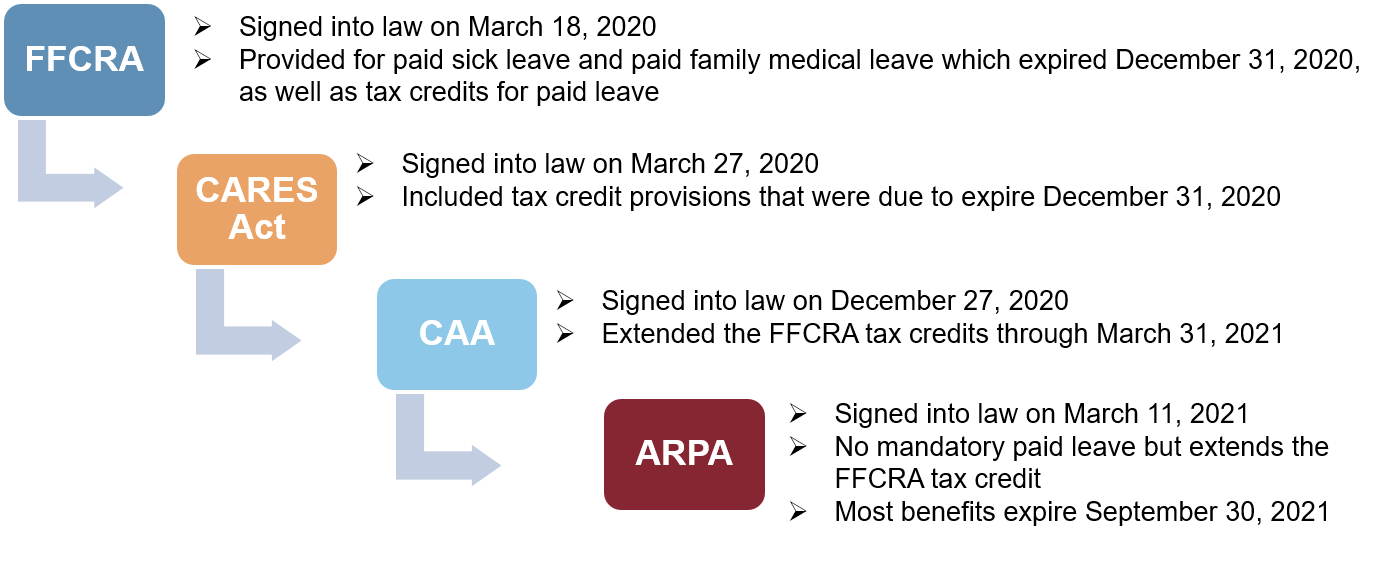

On March 11, 2021, President Biden signed the American Rescue Plan Act of 2021 (“ARPA”) into law as a response to the continuing effects of the COVID-19 pandemic and corresponding economic crises. This $1.9 trillion stimulus package provides, among other relief, adoption of a paid leave plan, funding for vaccinations, aid to working families, and support to businesses. This legal update provides some key features of this law that all employers should be aware of relating to employee leave and will be the first of other Eckert Seamans COVID-19 alerts discussing the ARPA.

Overview of COVID-related legislation:

THE ARPA AMENDS THE FFCRA

On March 18, 2020, Congress enacted the Families First Coronavirus Relief Act (“FFCRA”) pursuant to the Coronavirus Aid, Relief, and Economic Security (“CARES”) Act which was effective from April 1, 2020 through December 31, 2020. The FFCRA required all private employers with fewer than 500 full-time or part-time employees within the U.S. (“Covered Employers”) to provide temporary job-protected paid sick leave and paid expanded family and medical leave to employees unable to work or telework during the public health crisis (“Eligible Employees”) due to qualifying reasons related to the COVID-19 pandemic. Two types of emergency paid leave provisions were included in the FFCRA:

- The Emergency Paid Sick Leave (“EPSL”) Act, which required Covered Employers to provide up to 80 hours (two weeks) of paid sick leave to Eligible Employees who need to take leave from work for qualifying reasons; and

- The Emergency Family and Medical Leave Expansion (“EFML”) Act, which expanded leave available under the Family and Medical Leave Act (“FMLA”). The EPSL provided two weeks of paid sick leave. In comparison, EFML provided Eligible Employees with an additional ten weeks of paid family and medical leave at two-thirds of their regular wages to care for a child whose school or place of care is closed, or whose care provider is unavailable, due to a COVID-19 related reason. Note that even if an employee is eligible to take EFML leave, they may not be eligible for FMLA leave.[1]

Employers may deny leave if there is no work available. For a more detailed explanation, view our alert on DOL Paid Leave Regulations – Top Ten Takeaways.

The Consolidated Appropriations Act (“CAA”) enacted in December 2020 extended the above paid leave provisions of the FFCRA to March 31, 2021, at the employer’s option. However, employers are no longer mandated to provide and employees are not entitled to such leave beyond December 31, 2020. Participation is voluntary. The ARPA makes amendments to the CAA and the CARES Act.

KEY TAKEAWAYS OF THE ARPA

- Covered Employers are not required to provide any emergency paid leave pursuant to the ARPA.

This new relief bill does not require employers to provide emergency paid leave, instead making it optional for them to offer this benefit. Employers will want to consider the costs and benefits of whether to provide such leave voluntarily. These include:

- Taking advantage of payroll tax credit for providing paid leave (see bullet (3) below).

- Consistency and conformance with state paid leave laws (including those on the horizon).

- Reducing the risk of sickness spreading in the workplace and/or encouraging employees to get vaccinated. Note that some states might require a business to shut down in the event of an outbreak.

- The impact of such leave on your business is based on the number of workers working remotely and for how long they will be working remotely (or required to return to the physical office). Emergency paid leave is not available if an employee is able to telework.[2]

Covered Employers – those with 500 or fewer employees – may offer either paid sick leave or paid family and medical leave, or both (or neither). One advantage of offering paid sick leave is that employees can qualify for an additional ten days of paid sick leave even if they have used all or some portion of their original EPSL leave prior to April 1, 2021. However, if they have not exhausted their original EPSL leave, no leave is carried over to the new ARPA leave allotment. In other words, every employee’s paid sick leave balance is re-set and capped at ten days as of April 1, 2021 if the employer chooses to provide this ARPA benefit, and, as discussed below, employers can receive a tax credit for providing up to ten days of paid sick leave.

- The ARPA provides additional reasons for providing paid leave (i.e., paid sick leave and paid family and medical leave).

The FFCRA outlined six qualifying reasons due to which an employee was able to take leave pursuant to the EPSLA and EFMLA:

- The employee is subject to a federal, state, or local quarantine or isolation order related to COVID-19;

- A healthcare provider advised the employee to self-quarantine due to concerns related to COVID-19;

- The employee is experiencing COVID-19 symptoms and is seeking a medical diagnosis;

- The employee is caring for an individual who is subject to a quarantine or isolation order or has been advised by a healthcare provider to self-quarantine;

- The employee is caring for a child whose school or place of care is closed for reasons related to COVID-19;[3] or

- The employee is experiencing any other substantially similar condition specified by the Secretary of Health and Human Services in consultation with the Secretary of the Treasury and the Secretary of Labor.

The ARPA added three additional reasons as follows, for which an employee may take either paid family and medical leave or paid sick leave:

- The employee is obtaining a COVID-19 immunization;

- The employee is recovering from an injury, disability, illness, or condition related to the immunization; or

- The employee is seeking or awaiting the result of a COVID-19 test or diagnosis when the employee has either been exposed to COVID-19, or the employer has requested the test or diagnosis.

Therefore, under ARPA, employees may take paid leave for the above nine covered reasons listed in (a) – (i) above if the employer takes advantage of this paid leave plan pursuant to the ARPA regardless of whether the employer participates in either the paid leave or paid family and medical leave benefit, or both.

If an employer offers, and an employee takes, paid sick leave for reasons (a) through (c) or reasons (g) through (i) above, the maximum amount of compensation for “paid sick time” is $511 per day. For reasons (d) through (f), the maximum is $200 per day.

If an employer offers, and an employee takes, paid family and medical leave, the maximum amount of compensation for paid leave, taken for any of the above nine reasons, may not exceed more than $200 per day and $12,000 in the aggregate for each employee.

- Covered Employers who voluntarily provide emergency paid leave are eligible for tax credits.

The CAA extended the benefit of obtaining a refundable tax credit for employers who provided paid leave pursuant to the FFCRA to March 31, 2021. The ARPA extended and expanded the qualification for these benefits through September 30, 2021. Employers who choose to voluntarily provide paid sick or paid family leave as provided by the FFCRA[4] may receive refundable tax credits up to the above amounts for the above-nine stated reasons. Employers who select to participate in both the paid family medical leave and paid sick leave benefits may be eligible to obtain a tax credit for providing up to 12 weeks of paid family or medical leave, in addition to providing ten days of paid sick leave. The aggregate cap for paid family leave (which employers may receive tax credits for) increased from $10,000 to $12,000 with the ARPA. Employers should note that there will be no “double” tax benefit/credit – the tax credit is only permissible under either the paid sick leave or the paid family and medical leave provisions of the ARPA – not both.

Employee Retention Credit

Eligible employers may also claim the employee retention credit (or “ERC,” which was initially introduced under the CARES Act) equal to 50% of up to $10,000 in qualified wages paid from January 1, 2021 through June 30, 2021. The ARPA extends this tax credit for the third and fourth quarters of this year. This tax aspect will be covered more in-depth in an Eckert Seamans legal update to be published in the near future.

- Anti-discrimination Provision

Employers who decide to provide the ARPA benefit must abide by the new anti-discrimination provision to qualify for the tax credits. Employers who seek the tax credit must provide the benefit to all eligible employees. Employers cannot decide to offer the benefit to some classifications of employees and not others (i.e., full-time vs. part-time).

The Internal Revenue Service (IRS) and the Department of Labor have not yet published guidance on the ARPA. However, employers should remain alert for such guidance after the law’s effective date of April 1, 2021, and update any notices and forms regarding changes (if any) to the employer’s leave policies to avoid any perception of discrimination.

- COBRA Subsidies

The ARPA provides COBRA subsidies to “assistance eligible individuals” who experience involuntary terminations of employment (for reasons other than gross misconduct) or a reduction of hours. COBRA subsidies under the ARPA must be made available by group health plans subject to COBRA including self-funded and fully insured plans, multiemployer plans, and governmental employer plans. Subsidies must also be made available by state programs that provide comparable continuation coverage (for smaller employers with less than 20 employees). This subsidy is equal to 100% of the applicable COBRA premium and applies to COBRA coverage in effect from April 1, 2021 through September 30, 2021.

Assistance Eligible Individuals

There are two categories of assistance eligible individuals. The first includes employees or former employees with involuntary terminations or reductions of hours who have elected and are receiving COBRA coverage from April 1, 2021 through September 30, 2021. The second category includes individuals who previously experienced involuntary terminations or reductions of hours but did not elect COBRA, or those who elected and subsequently dropped COBRA coverage, and who are still within their COBRA maximum coverage period. This second category of individuals must be given a second chance to elect COBRA to take advantage of the subsidy. For this second category of assistance eligible individuals the new COBRA election does not extend the COBRA period beyond the date it would otherwise have expired. Employees who voluntarily terminated their employment are not eligible for the subsidized coverage.

Notice Requirement

Employers will be required to send a notice to each “assistance eligible individual” by May 31, 2021 to notify them of their new rights. Assistance eligible individuals will have a special election period until 60 days after receipt of the notice to make an election. The Department of Labor has issued relevant guidance and model notices for plans to provide the notice and special election period.

Like the other benefits under the ARPA, the premium assistance ends on September 30, 2021, but cuts off sooner if (1) an individual becomes eligible to enroll in certain other group health plan coverage or Medicare or (2) the individual’s COBRA coverage period expires.

Employers. will offset the cost of the COBRA subsidy by claiming a credit against its quarterly Medicare payroll taxes. [5] If the credit exceeds the employer’s Medicare payroll tax, the excess will be treated as an overpayment and fully refundable.

[1] The FMLA only requires employers to provide unpaid leave.

[2] An employee is able to telework if:

- his or her employer has work for the employee to perform;

- the employer permits the employee to perform that work from the location where the employee is being quarantined or isolated, or caring for a family member; and

- there are no extenuating circumstances that prevent the employee from performing that work. 29 CFR § 826.10.

[3] Previously, this was the only reason an employee was able to take paid family and medical leave. Effective April 1, 2021, the covered reasons for taking such leave are expanded to the nine reasons discussed in this alert.

[4] In the ARPA provisions pertaining to tax credits, “qualified sick leave wages” is defined as the wages that would be paid by reason of the EPSL Act as if applied after March 31, 2021, and “qualified family leave wages” is defined as wages that would be paid by reason of the EFML Act as if applied after March 31, 2021. Thus, employers that choose to voluntarily provide either/both of those two types of FFCRA leave will be eligible to receive refundable tax credits.

[5] Under Section 6432 of the ARPA, for state continuation coverage applicable to small employers with 20 or fewer employees, the tax credits reimbursements would apply to the insurer.

Click here to view a downloadable PDF of the legal update.

This Alert is intended to keep readers current on developments in the law and is not intended to be legal advice. If you have any questions, please contact members of Eckert Seamans’ Labor & Employment or Employee Benefits groups or any attorney at Eckert Seamans with whom you have been working.